12 Oct Are You on a Medicare Cliff? Finding Out Can Save You Money.

If you are on Medicare, but have a higher income level, you might be on the edge of a “cliff” without knowing it.

What is a Medicare cliff?

Medicare Part B monthly premiums are what you pay each month to have coverage. Premiums are based on your income level from 2 years ago. If you earn more than $88,000 as an individual, or $176,000 with your spouse, you will have to pay an income-related monthly adjusted amount (IRMAA) on top of your Medicare Part B premium. This means that an increase in income, even as little as $1, could push you over your current income bracket for Medicare premiums. This results in a significantly higher premium. In other words, pushing you off an income-based “cliff.”

How much can $1 really matter when you're on the edge of a Medicare Cliff?

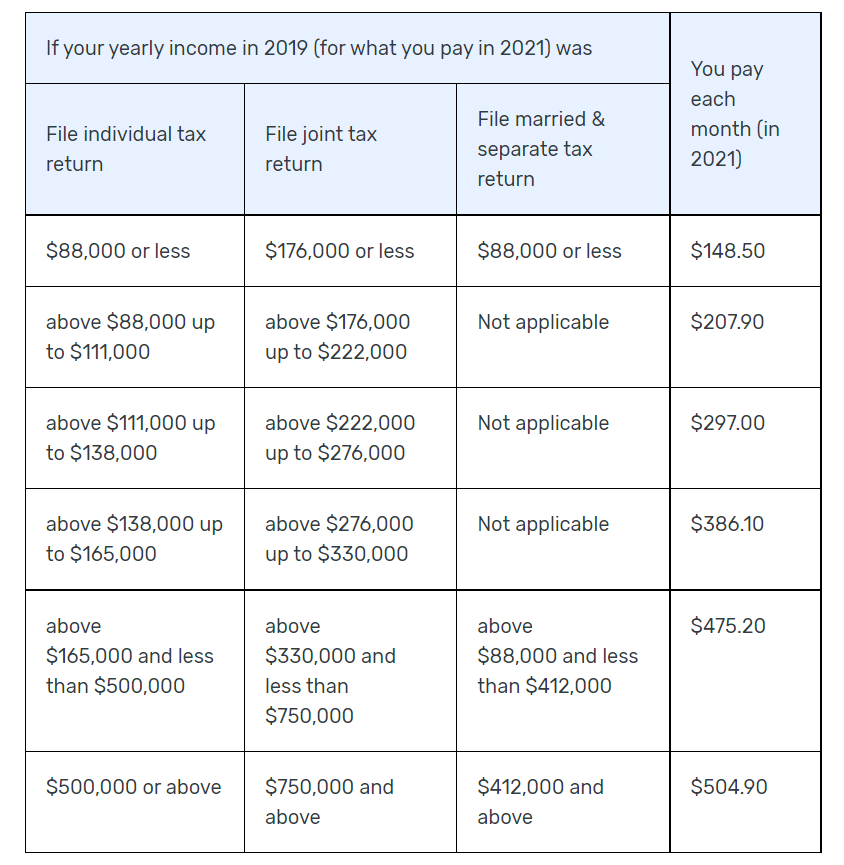

Medicare Part B Premiums. Source: Centers for Medicare and Medicaid Services.

For individuals who earned more than $88,000 (and couples earning $176,000) on their most recent tax return, premiums for Medicare Part B range from $207.90 and $504.90.

Where your premium falls in this range could come down to the dollar.

If you and your spouse made $176,000 in 2019, your premium would be $148.50 in 2021, or $1,782 a year. But, if you increased your income to $176,001 and jumped off the Medicare “cliff,” your monthly premium for Medicare Part B will be $207.90 for 2021, or $2,494.80 per year.

This means earning one dollar more per year could cost you a 40% increase in your Medicare Part B premiums.

Are Medicare Part D premiums also based on income?

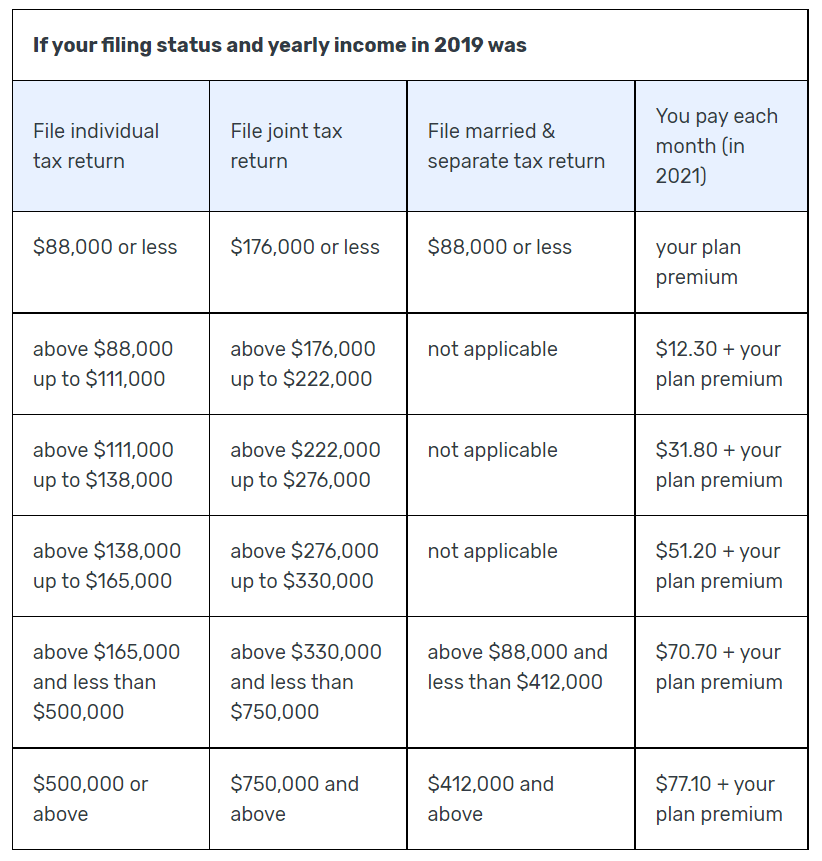

Yes. Medicare Part D premiums depend on the plan you choose. But, if your income is higher than $88,000 (or $176,000 for you and your spouse) on your 2019 tax return, you will have to pay an additional amount on top of your monthly Part D plan premium.

For example, if you and your spouse earned $176,000 in 2019, you would only have to pay your plan’s Medicare Part D premium. In 2021, average Part D plan premiums cost about $33 per month. For one year of coverage, you would pay $396.

But, if you earn only a dollar more ($176,001) you are over the edge of the Medicare cliff and you’ll have to pay an additional amount of $12.30 per month. This means your yearly costs for Part D premiums will be $543.60, or 37% higher than if you earned $1 less.

Just like for Part B, raising your income by $1 could raise your Part D premiums by nearly 40%.

How can you protect yourself from increased premiums this year?

If you’re worried about increased premiums and your 2019 income tax return does not reflect your current income, you can ask the Social Security Administration to reduce or eliminate your IRMAA. Reasons the SSA will reconsider your IRMAAs include:

- Change in marital status (new marriage, divorce, or death of a spouse)

- Loss of pension

- Stopping work or reducing hours

Make sure to gather and submit documents to support your appeal (e.g., your new work schedule and pay stubs if you reduced work hours). To appeal your IRMAAs, fill out this form or visit HHS.gov.

Medicare Part D Premiums. Source: Centers for Medicare and Medicaid Services.

What about this year’s income tax return?

While income brackets will change year-to-year, strategically lowering your income for your 2021 tax return can protect you from a higher premium in 2023.

There are a few ways you may be able to lower your income:

- Increase your retirement contributions: By increasing the percentage of your paycheck you contribute to an individual retirement account (IRA) or 401(k), you can lower your income for 2021, while keeping these funds for the future.

- Increase your Health Savings Account (HSA) Contributions: HSAs are similar to personal savings accounts, but the money in the account is only used to pay for certain health care costs, and is tax-free. You could deposit income that might push you off the Medicare cliff into an HSA, and use the money to pay for health care expenses. In order to be eligible for an HSA, you must be under the age of 65 and have a high-deductible health insurance plan. You can start your own HSA through a financial institution, or your employer may offer an option for an HSA.

- Make charitable distributions from IRAs: If you would like to reduce your income while supporting causes that matter to you, you can reduce your yearly income by making tax-free donations from your IRA. To make these tax-free gifts, you must be at least 70 ½ years old and be the IRA trustee of a traditional IRA or Roth IRA (this excludes accounts like 401(k)s).

- Realize Capital Losses: You may have some assets in the form of stocks or other taxable investment accounts. In that case, realizing capital losses, or keeping track of any dips in the value of your investments, can help keep your income lower. You can talk to an accountant to learn more about lowering your income level.

If you are having trouble keeping up with your Medicare premiums, Triage Cancer is here to help.

See our Quick Guide to Medicare Savings Programs for information on financial assistance to pay for Medicare. For more information on Medicare, visit CancerFinances.org.

Triage Cancer is a national, nonprofit providing free education to people diagnosed with cancer, advocates, caregivers, and health care professionals on cancer-related legal and practical issues. Through events, materials, and resources, Triage Cancer is dedicated to helping people move beyond diagnosis.

Similar Posts You May Like To Read:

- Paying Too Much for Medicare? How to Lower Your Premiums

- Medicare Open Enrollment is Here – How to Avoid Late Enrollment Penalties

- Saving Money with Medicare Part D

- Can a Health Savings Account (HSA) Help You?

- Medicare Enrollment Periods – Do You Know the Difference?

- How Does the Inflation Reduction Act of 2022 Affect You?

- Have Medicare and an HSA? Don’t make a costly mistake!

- Need Help with Prescription Drugs? Medicare's Extra Help Program Offers Relief