Quick Guide to Co-pay Accumulators and Maximizers, & Alternative Funding Programs

In Triage Cancer’s free Quick Guide to Co-pay Accumulators and Maximizers, & Alternative Funding Programs, you’ll learn about co-pay assistance, accumulators and maximizers, alternative funding programs, how these programs affect your out-of-pocket costs, how to find out if your plan uses them, and more.

")

")

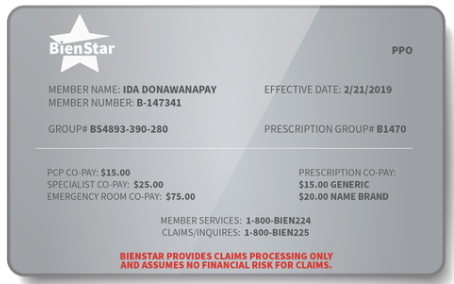

loyee may have an insurance card with the logo of an insurance company, but it is the employer that is assuming the cost of claims. See this sample insurance card with self-insured language in red.

loyee may have an insurance card with the logo of an insurance company, but it is the employer that is assuming the cost of claims. See this sample insurance card with self-insured language in red.