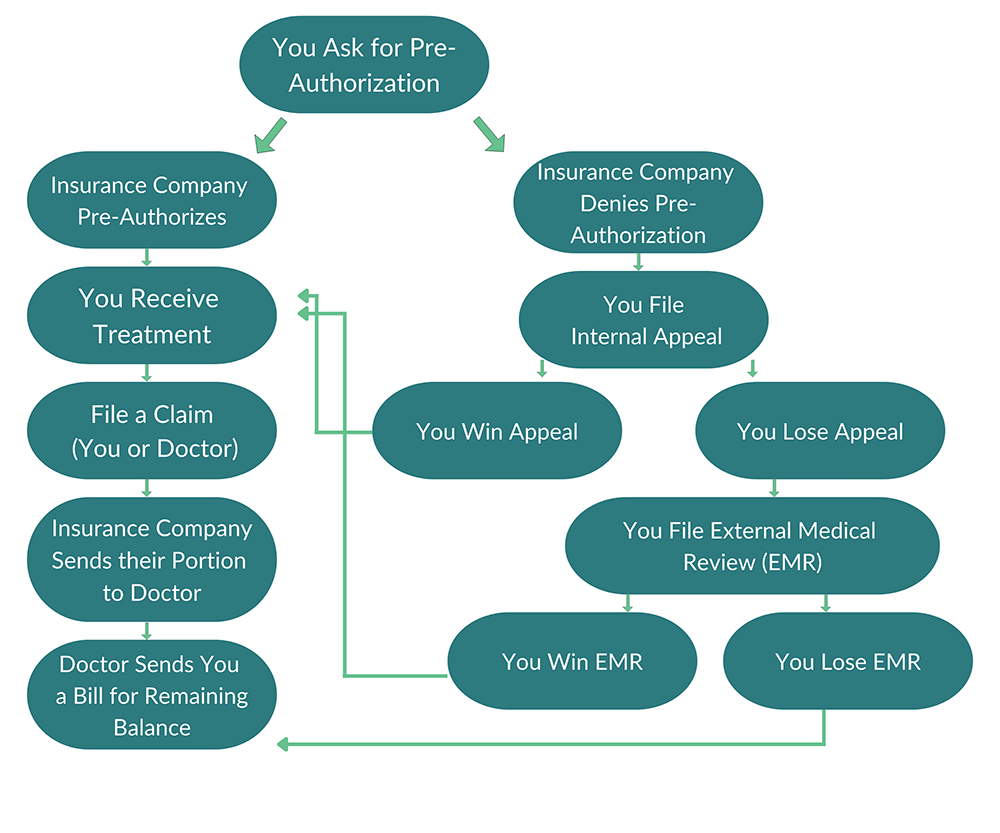

What is a Pre-Authorization?

Health insurance companies may require you to obtain their written approval before you receive certain medical care, including specific treatments, medical devices, and prescriptions. This approval is called preauthorization, but might also be called pre-auth, prior authorization, prior auth, prior approval, precertification, treatment authorization request, or advanced approval.

Insurance companies are not required to pay for medical care that requires pre-authorization, if a patient receives these services without the pre-authorization. Patients may then have to pay the full cost of the medical care. Medical care that might require pre-authorization includes:

- Medical treatments that have lower-cost, but equally effective, alternatives available

- Medical treatments and medications that should only be used for certain health conditions

- Lab tests, imaging scans, and biomarker tests

- Medical treatments and medications that are often misused or abused

- Medications that may be unsafe when combined with other medications

- Drugs often used for cosmetic purposes

- Medical care that is provided out-of-network

Most insurance companies do not provide a list with the medical care that requires a pre-authorization, so you have to ask. Your insurance company may also change its pre-authorization requirements at any time.

Sometimes, your health care team will request a pre-authorization for you. But if they don’t, and you get the medical care without the pre-authorization, then your insurance company may refuse to pay for the care.

Ultimately, it is the patient’s responsibility to get the pre-authorization. This means that it is always helpful to ask your health care team if they will be getting any necessary pre-authorizations for you. If they aren’t, then you need to get the pre-authorization from your insurance company.