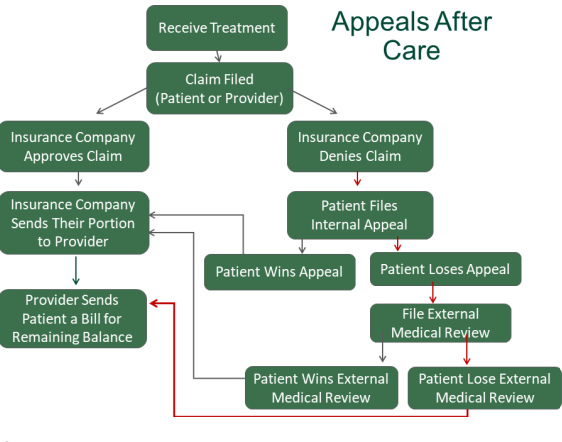

Internal vs. External Appeals

You generally have two chances to appeal a denial of coverage: an internal appeal and an external appeal.

Internal Appeals: When an insurance company has denied coverage for care, you can file an “internal appeal” within your insurance company. Each insurance company has their own internal appeals process, so contact your insurance company for details or look for instructions on how to file an appeal on your denial letter. There are time frames related to filing an internal appeal.

If your insurance company denies your internal appeal, you can request an external appeal. Under the Affordable Care Act, all states must have an external appeals process – this is also sometimes referred to as External Medical Review or Independent Medical Review.

External Appeals: Within four months of receiving your insurance company’s denial of your internal appeal, you can file a written external appeal (note some states provide additional time). External appeals are completed within 45 days of filing and the decision is binding on the insurance company. If urgent, reviews can be expedited, filed at the same time as an internal appeal, and decided within 72 hours. State insurance agencies or the federal Dept. of Health & Human Services administer external appeals. To find the process and contact information for your state, see our free State Resources. The HHS process is free, but states can’t charge more than $25 for an external appeal.